AWS for Industries

Coins in Motion: Building agentic blockchain payments for in-vehicle experiences

Agentic blockchain-based payments are poised to transform in-vehicle driving experiences. As vehicles become increasingly connected and autonomous, they are evolving from passive transportation tools into active economic agents capable of conducting their own financial transactions [see HBR Article, 2021]. Imagine your car automatically paying for highway tolls, electric charging sessions, parking fees, or even purchasing real-time traffic data, all without human intervention. In this post, we describe how this vision can become reality through blockchain-based micro-payment systems that enable vehicles to transact autonomously, efficiently, and securely. Specifically, we introduce a solution design and show how this can be applied to implement three exemplary use cases, namely agentic 1/ road toll, 2/ vehicle charging, and 3/ in-vehicle entertainment payments.

Traditional payment infrastructure was never designed for the machine economy. Credit card processors charge 2–3% per transaction, making payments under a few dollars economically unviable. Banks operate on business-day schedules with settlement times measured in hours or days, creating friction for time-sensitive transactions. These limitations have constrained innovation in connected mobility services, forcing providers to bundle charges or require prepayment, both creating poor user experiences.

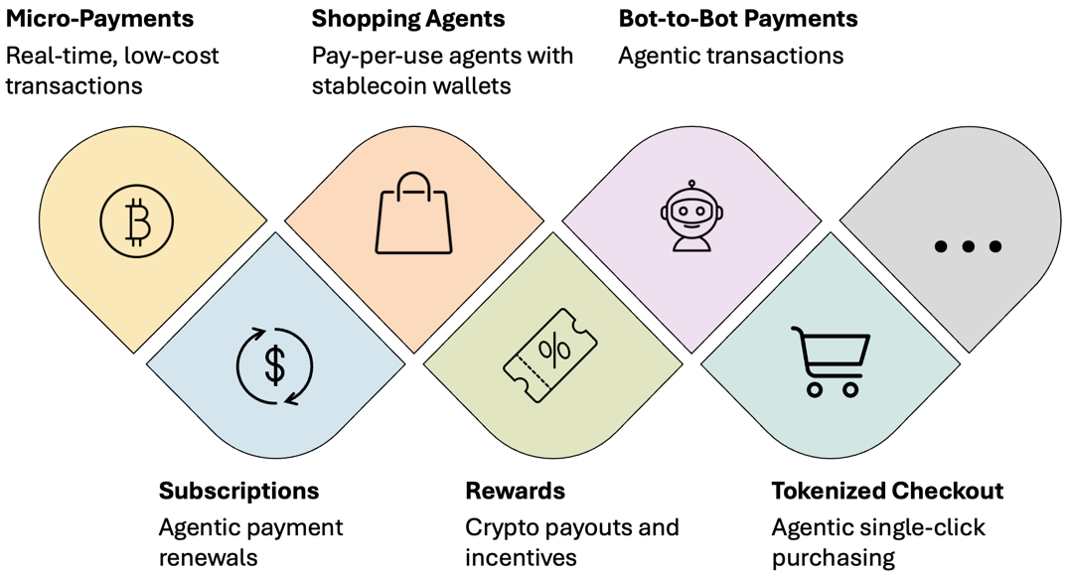

Blockchain technology fundamentally re-imagines this paradigm and enables various use cases such as micro-payments, shopping agents, and bot-to-bot payments as depicted in Figure 1. By using stablecoins [see e.g. HBR Article, 2024] – digital currencies pegged to fiat money like dollars or euros – vehicles can conduct micro-payments with transaction costs measured in cents rather than percentages. A car can pay $0.15 for 5 minutes of parking or $0.03 for a single toll crossing, with fees that make such granular transactions economically sensible for the first time.

Foundational concepts

Understanding how blockchain technology enables this payment transformation requires grasping several interconnected concepts:

Distributed ledger: A blockchain is a shared digital ledger distributed across thousands of computers worldwide. Rather than relying on a single entity like a bank to maintain records, every participant holds an identical copy. Data is organized into sequential blocks, each cryptographically linked to the one before it, making historical records practically impossible to alter.

Cryptographic key pairs: Users are identified through cryptographic key pairs. A public key serves as your visible account address, while a private key proves ownership and authorizes transactions. This “self custody” model enables true machine autonomy. Vehicles can hold and manage their own payment accounts without requiring human authorization for each transaction.

Smart contracts and stablecoins: Smart contracts are self-executing programs that live on the blockchain. They automate complex payment logic, releasing funds only when charging is complete, automatically converting between currencies when crossing borders, or splitting payments among multiple parties instantly. Smart contracts also enable stablecoins, digital currencies pegged to traditional money like US dollars or euros. Unlike volatile cryptocurrencies, stablecoins maintain predictable value, making them suitable for everyday payments.

24/7 settlement and Layer 2 networks: Blockchain networks run 24/7 and settle transactions in seconds to minutes, enabling real-time payments at highway speeds. Layer 2 networks further improve efficiency by processing transactions off the main blockchain while inheriting its security, reducing fees from several dollars to mere cents and making cross-currency conversion between stablecoins (for example, euro-backed to Swiss franc-backed) far simpler than traditional foreign exchange.

Figure 1: Exemplary use case categories enabled by agentic, blockchain-based payments.

These technical foundations combine to create an infrastructure purpose-built for the machine economy, where vehicles become autonomous economic agents that address real friction points in today’s connected vehicle environment.

Use case 1: Road toll payments

Road tolling represents one of the most complex payment scenarios in transportation. A single cross-border journey can involve multiple stakeholders: toll operators, law enforcement agencies, customs authorities, and government entities across different jurisdictions, each requiring accurate records of passage, payment, and compliance. Today’s fragmented landscape creates significant friction. The European Union’s European Electronic Toll Service (EETS) was established specifically to address interoperability challenges, aiming for “one contract, one on-board unit” across countries and toll systems. Yet drivers still face incompatible payment systems, unclear pricing across borders, and the administrative burden of managing multiple accounts or devices. Agentic payments reduce this complexity. When a vehicle approaches a toll point, its payment agent can automatically:

- Generate privacy-preserving proof-of-passage by creating a cryptographic hash combining the license plate, timestamp, and toll domain identifier

- Make instant micro-payment for the exact toll amount in the appropriate local currency (automatically converting between euro-backed and Swiss franc-backed stablecoins, for example)

- Maintain compliance records on-chain while keeping personally identifiable information off-chain, satisfying both regulatory requirements and privacy concerns

- Enable multi-party settlement where the smart contract automatically distributes funds among toll operators, government agencies, and infrastructure maintenance budgets according to pre-defined rules

The vehicle becomes its own payment agent, handling the entire transaction autonomously while the driver focuses on the road. Instead of purchasing an e-vignette or sticker that needs to be attached to the vehicle’s windscreen, the road toll payment agent automatically processes the payment.

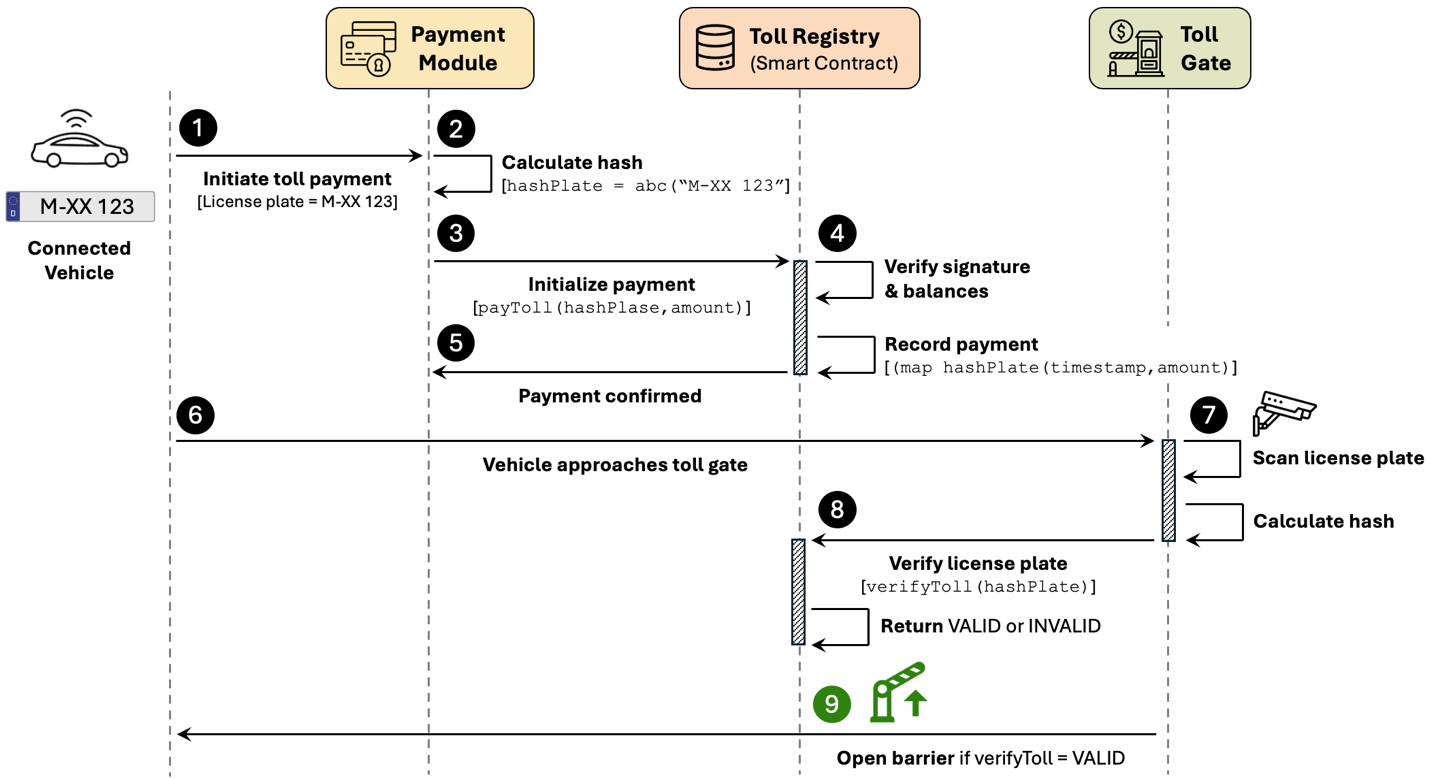

As the vehicle approaches Switzerland from Germany, for example, the agent is aware of the current location on the German autobahn and checks for a valid e-vignette. The agent can discover all required parameters, such as the “Toll Registry” smart contract address from the Swiss authority. If the agent discovers that no e-vignette has been purchased for the current year, it triggers the following workflow depicted in Figure 2:

Figure 2: High-level process flow for the agentic toll payment use case based on nine steps (1-9).

- The agent initializes the toll payment process by using the license plate “M-XX 123” as an identifier.

- The in-car payment module calculates the hash value to protect privacy. The hash value can either be the license plate number or a more privacy preserving option, such as static hashing by using salts or zkproofs, for example.

- The agent then initializes the payment using a stablecoin, such as a digital euro.

- The blockchain validates the “signature” and “balances” submitted by the in-car payment module and records the payment.

- The in-car payment module receives confirmation of the purchase.

- The vehicle continues to approach the toll gate.

- A camera along the way scans the license plate and creates a hash value based on it.

- The calculated hash value from the camera is verified against the toll registry.

- The barrier at the toll gate opens if the verification is successful.

The next time the vehicle approaches Switzerland via autobahn, for example entering from Italy, the agent checks again and finds a valid “e-vignette” independent from the driver. Such an agentic system is flexible and can be adapted to support different types of tolls for example “toll roads” in the United States or “vignettes” with different expiry (1 day, 10 days, 2 months, 1 year) such as in Austria.

For fleet operators and rental car companies managing hundreds of vehicles across multiple countries, this agentic toll payment process reduces manual reconciliation effort. Every toll passage is recorded immutably with cryptographic proof, automatic currency conversion, and instant settlement. Law enforcement retains the ability to verify compliance when needed, but routine toll collection doesn’t create a surveillance trail of every vehicle movement.

Solution architecture for use case 1: Road toll payments

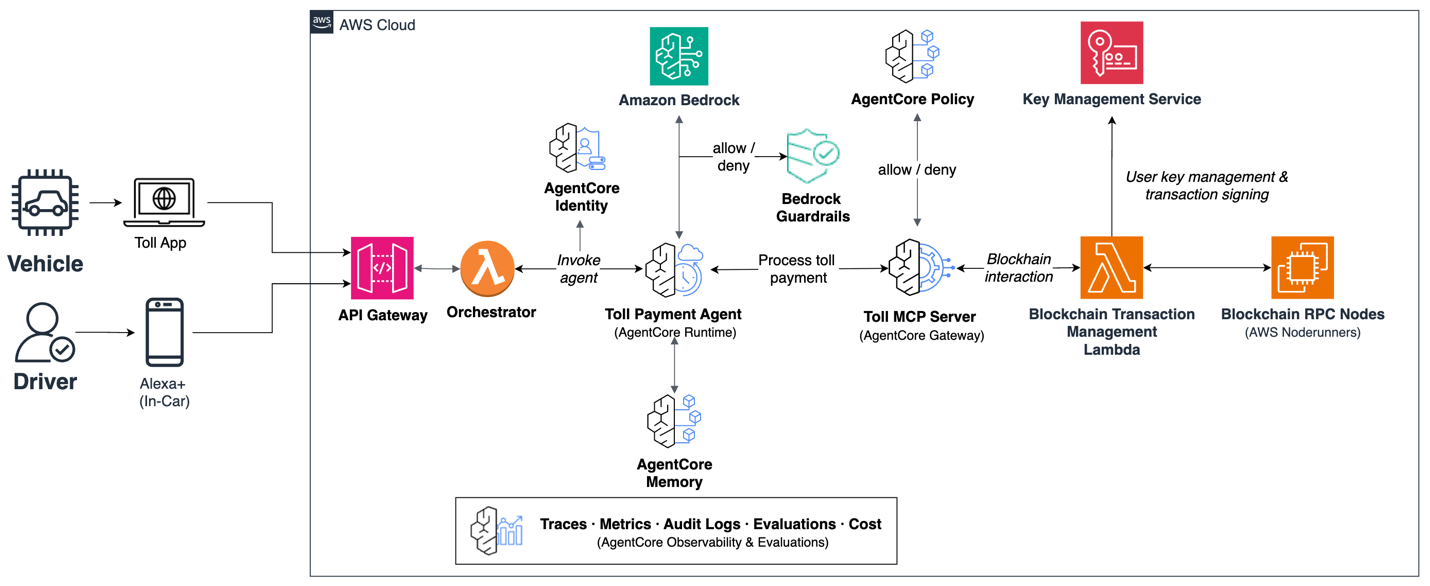

Figure 3: AWS solution design for the agentic toll payment use case.

Figure 3 illustrates a complete solution design for this agentic toll payment use case, built on Amazon Bedrock AgentCore. The architecture enables a vehicle to autonomously detect, authorize, and settle toll payments on a blockchain. It supports two input channels, namely a toll application (Toll App) running on the vehicle’s onboard unit, and an in-car voice assistant, such as Alexa+ [see Amazon Website, 2026]. Both submit payment requests through Amazon API Gateway, which routes them to an orchestrator AWS Lambda function responsible for request validation and agent invocation.

At the core of the architecture sits the Toll Payment Agent, hosted on the Amazon Bedrock AgentCore Runtime. This agent reasons about incoming toll events by invoking a foundation model on Amazon Bedrock, for example to determine the correct toll tariff based on vehicle class, time of day, and jurisdiction. Amazon Bedrock Guardrails wraps the model interaction, applying content filtering and contextual grounding checks to ensure the agent’s reasoning stays within the toll payment domain and its outputs remain grounded in the provided context. This prevents scenarios where the model drifts off topic, leaks sensitive information such as license plate data in its responses, or produces ungrounded toll amounts that do not correspond to actual tariff schedules. Amazon Bedrock AgentCore Identity authenticates callers before the agent is invoked and provides the credential context the agent carries through downstream calls.

When the agent determines that a payment should be made, it issues a Model Context Protocol (MCP) tool call to the Toll MCP Server, hosted on the Amazon Bedrock AgentCore Gateway. Amazon Bedrock AgentCore Policy enforces authorization rules at this boundary, validating whether the agent is permitted to invoke the requested tool and whether the transaction falls within pre-configured spend limits. The MCP Server then triggers the Blockchain Transaction Management Lambda, which constructs, signs, and submits the on-chain transaction. Private keys are managed through AWS Key Management Service (AWS KMS), ensuring cryptographic material never leaves a secure boundary. The transaction is submitted to blockchain Remote Procedure Call (RPC) nodes operated through AWS Blockchain Node Runners.

AgentCore Memory provides the agent with persistent context across sessions, for example remembering a vehicle’s toll history or preferred payment currency. A cross-cutting AgentCore Observability layer captures traces, metrics, audit logs, and cost data across the entire agentic flow, from agent invocation through tool execution to blockchain settlement. This telemetry feeds into AgentCore Evaluations, which assesses agent quality, payment accuracy, and guardrail effectiveness over time.

This solution design can also be used principally to support two further use cases, namely vehicle charging and in-vehicle entertainment payments, each of which is described in more detail in the following sections.

Use case 2: Vehicle charging payments

Electric vehicle (EV) charging is rapidly evolving toward frictionless experiences. Modern electric vehicles can already identify themselves to compatible chargers automatically through standards like ISO 15118. ISO 15118 is an international standard defining vehicle to grid (V2G) communication interface for bi-directional charging/discharging of EVs. The standard provides multiple use-cases like secure communication, smart charging and features such as “Plug & Charge”. Charging networks furthermore are improving interoperability, so drivers can access multiple providers with a single account. Agentic payments complete this vision by making the financial transaction as seamless as the physical connection. When a driver plugs in their vehicle, the charging session becomes a continuous micro-payment stream:

- Session initiation happens automatically as the vehicle and charger authenticate through cryptographic handshake

- Pay-as-you-charge micro-payments flow in real-time as energy is delivered—paying per kilowatt-hour rather than pre-authorizing large amounts on a credit card

- Dynamic pricing adaptation where the smart contract adjusts rates based on time-of-day pricing, grid demand, or renewable energy availability

- Automatic fee reconciliation that calculates energy costs, time-based fees, and idle penalties, settling the final amount instantly when the driver unplugs

This approach eliminates common pain points: no more juggling multiple charging network apps, no pre-authorization holds tying up credit limits, no surprise bills days later, and no confusion about pricing across different networks or countries. For charging infrastructure operators, agentic payments reduce payment processing costs – from 2-3% credit card fees to fractions of a cent per transaction. The 24/7 settlement capability means revenue is recognized instantly rather than waiting for batch processing, improving cash flow. Smart contracts can even enable innovative business models like dynamic load balancing, where vehicles agree to slower charging rates in exchange for lower prices during peak demand periods.

The system maintains a complete, tamper-proof record of every charging session: energy delivered, time connected, pricing applied, and payment settled. This transparency benefits all parties—drivers can verify they paid fair rates, operators can prove service delivery, and regulators can monitor market behavior without intermediaries controlling the data.

Use case 3: In-vehicle payments

Modern vehicles are rapidly becoming entertainment platforms with embedded app stores, streaming services, and subscription bundles integrated directly into cabin interfaces. This “app economy on wheels” creates new opportunities but also new friction: account management across multiple services, payment authorization while driving, and determining whether purchases belong to the driver, a passenger, or a fleet policy.

Agentic payments integrate in-vehicle commerce directly into the cabin experience while enforcing safety controls. The vehicle’s payment agent can:

- Make context-aware purchases like buying a one-time movie rental for rear-seat passengers during a long trip, unlocking a weekend “premium streaming” pass, or paying per-minute for content during a charging stop

- Enforce safety policies automatically through smart contracts that only enable video playback when the vehicle is parked or when certified hands-off autonomous driving mode is active

- Manage multi-user scenarios where different passengers can make purchases from their own wallets without sharing payment credentials with the vehicle owner

- Enable granular monetization for content providers – charging $0.50 for a single song, $2 for a 30-minute podcast episode, or $5 for a feature film, with transaction costs low enough to make micro-pricing economically viable

This aligns with where automotive OEMs are heading, namely subscription-based digital services and commerce flows integrated directly into the cabin user interface. Rather than forcing drivers to create accounts, remember passwords, or enter payment details while on the road, the vehicle handles transactions autonomously based on pre-set preferences and spending limits. For families, this creates new possibilities: parents can give children a monthly entertainment budget stored in the vehicle’s wallet, with smart contracts automatically enforcing spending limits and content restrictions. For fleet operators, corporate policies can be encoded directly, allowing drivers to expense certain content categories while blocking others, with automatic reporting for accounting purposes. The blockchain foundation ensures transparency and auditability: every purchase is recorded immutably, making it easy to review spending, dispute charges, or demonstrate compliance with corporate policies. Content providers benefit from instant settlement and dramatically reduced payment processing costs, enabling new business models that weren’t economically feasible with traditional payment rails.

Conclusion

The automotive industry is changing, with vehicles evolving from passive transportation tools into autonomous economic agents. By combining blockchain technology, stablecoins, and smart contracts, agentic payment systems eliminate the friction of traditional financial infrastructure—enabling seamless micro-transactions for road tolls, EV charging, and in-vehicle entertainment. Built on robust architectures like Amazon Bedrock AgentCore, these solutions can provide security, transparency, and real-time settlement. As connected and autonomous vehicles become mainstream, agentic blockchain-based payments can reshape how vehicles and commerce interact and support new machine-economy use cases.