AWS for Industries

How payment companies are using cloud technology to respond to shifts in consumer behavior

COVID-19 has upended the way consumers interact with their financial institutions on an unprecedented scale and speed as detailed in the blog post authored by Scott Mullins, Managing Director of Worldwide Financial Services Business & Market Development for AWS, and the payments industry is no exception.

The global pandemic has accelerated the growth of digital payments, peer-to-peer (P2P) networks and cashless transactions as homebound shoppers purchase groceries and medicines, and retail stores offer contactless shopping; P2P payment networks like Venmo and Paypal are also increasing spending limits and easing rules for certain transactions.

Although the shift to digital was already underway before the crisis, payment providers are now seeing a dramatic acceleration of three key trends: the need to scale processing, rising fraud attempts related to digital engagement, and an opportunity to adapt to changing lending and credit evaluations.

Scaling payment processing in response to the surge in digital transactions

With digital payments and transaction volumes growing across the globe, one of the main advantages of moving to the cloud is the ability to preempt and automatically address spikes in payment processing. For payment companies, the sudden surge in demand calls into question the ability of a company to allocate resources to handle the heaviest predicted uptick in transactions without a degradation in performance.

Prior to the pandemic, a number of companies gained a competitive advantage by planning for capacity and flexibility upfront. We can learn from firms like FinTech startup Affirm, a point of sale installment lender that effectively managed spikes in transactions. Back in 2018, Affirm prepared for a massive influx of activity during the critical holiday period by building a scale-up, fault tolerant, database system in AWS that was able to handle 5x their typical daily volume. Another example we can look to is Klarna Bank, a Swedish FinTech founded in 2005 that provides payment solutions for 85 million consumers across 205,000 merchants in 17 countries. Before the health crisis, Klarna built a core banking platform on the cloud that has enabled them to scale in order to meet increased demands and changing customer behaviors. As the “pay later” partner of choice for the top 100 highest grossing merchants in the U.S., Klarna’s platform supports +1M daily transactions in a smooth one-click purchase experience that lets consumers pay when and how they prefer to.

Digitally engaging customers, while protecting against heightened risk and fraud

Maintaining effective contact centers has never been more urgent to continue personalized interaction with customers even when bank branches are closed. Many financial institutions are using Amazon Connect, an easy to use cloud-based contact center that scales to support businesses of any size, to improve customer experience. One example is a large payment processor that now takes 6,000+ calls/day with Amazon Connect’s open platform that has been integrated with the processor’s own switchboard application. By making the switch to Amazon Connect, the company ensures customers are sent to the right agents based on availabilities and skill sets to efficiently resolve issues.

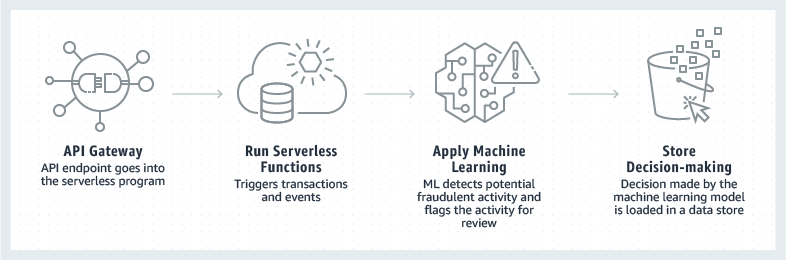

Unfortunately, fraud thrives in times of fear and uncertainty and fraudsters are likely to attack during times of increased remote or online transactions. In March, the FBI issued a public service announcement and warned against a rise in fraud schemes related to the pandemic. To help account holders monitor against these instances of fraud, we are helping customers use Multifactor Authentication (MFA) with traditional authentication methods such as one-time-passwords, real-time alerts, and use notifications to help clients track account activity and report suspicious activity immediately. Payments companies can use AWS services such as Amazon Pinpoint to power these and other mission-critical communications workloads.

AWS is also helping customers prevent fraud while maintaining frictionless purchasing experiences with newer authentication techniques. For example, we can learn from how Mastercard’s NuData uses passive biometrics to authenticate account holders’ identities by analyzing their digital profiles—behaviors that can’t be replicated by another party. Built on a data lake, petabytes of customer data are collected and analyzed in real-time. Working with AWS has enabled NuData to move from focusing on infrastructure to developing customer solutions and critical innovation.

How to Prevent Fraud Using Machine Learning on AWS

Adapting to changing lending and credit evaluations

Financial institutions have the opportunity to help consumers and small businesses weather the economic storm by providing the cash or liquidity they need during this time of volatility. Many lenders use a data-driven approach to understand which customers need help. Some payment companies are rapidly adapting to respond to urgent consumer needs. As shown in recent press or earnings announcements, Synchrony Financial says it is reevaluating credit card limits “dynamically” with internal and credit bureau triggers; and Discover says it is also evaluating creditworthiness on “continuous” basis.

The full economic impact of the pandemic remains uncertain. What used to look like a “good” credit score is likely to be aspirational for many individuals. As a result, financial institutions are looking for new ways to use real-time analysis that leverages updated or new algorithms to help extend new credit lines, while balancing speed with security and quality underwriting decisions. With AWS, payments and lending companies are better positioned to use new or alternative data types, streaming data, data lakes, and machine learning to help make rapid credit decisions, reach new consumers, and deliver on changing expectations. Although payment companies need to recognize the likelihood of defaults over an extended period and respond with diligent credit checks, there is significant opportunity to help customers before these individuals default.

A company that has been using new types of data in innovative ways is CreditVidya, a startup headquartered in India whose underwriting technology is opening the country’s loans market to over 250 million financially excluded citizens. To determine creditworthiness, CreditVidya’s ML platform leverages payment data, financial behavioral data, and device data stored on smartphones to help determine loan applicants’ ability and intent to repay loans.

How to Extend Credit Using AWS Tools

The long term challenge for payment firms: driving consumer spend while staying nimble and dynamic

Credit card companies are driving news ways for customers to spend. To encourage continued use of their cards, loyalty and reward points are being aligned with consumer purchase patterns, such as online groceries, food delivery, streaming services, even allowing rewards to be used for charity donations. Major U.S. card issuers raised the threshold for contactless payments while Stripe, the San Francisco digital payment platform popular with Shopify, Instacart and other major online retailers, announced updates to its software to connect users directly to the world’s six major global credit card systems.

Companies are looking for ways to change direction or pivot their business models effectively with the help of technology. In April, Kabbage, Inc. became the first FinTech to enable tens of thousands of small businesses to submit Paycheck Protection Program (PPP) loan applications in minutes using automation tools like Amazon Textract. With over 10 years of specializing in analyzing, verifying and approving high volumes of small business lending applications, Kabbage restructured its technology in less than one week to allow any U.S. small business to apply for financial relief appropriated in the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

As a result of social distancing and other pandemic-mitigation measures, there’s no question the health crisis has altered consumer spending and fast-tracked digital transformation in payments. The whole payments value chain – managing the entire payment flow from checkout through to final settlement – will continue to evolve according to how and where consumers interact with their financial institutions. As firms advance digital initiatives to modernize payments, there is tremendous opportunity to leverage the benefits of the cloud and AWS technology solutions to scale processing, improve customer experience, and extend credit to individuals who may need it the most.

For more information about the AWS solutions mentioned above or how to work with us, please contact your AWS Account Manager or visit AWS Financial Services. You can also read about Amazon’s actions to support those directly and indirectly impacted by COVID-19, by visiting Amazon’s Day One Blog and AWS Initiatives and Response to COVID-19.