AWS Startups Blog

VC 101: how VCs operate, and what you should know as a founder

By Drew Russ, VC BDM, AWS

Drew Russ, AWS Startup & Venture Capital Business Development Manager, held sessions at the AWS Pop-up Lofts in San Francisco and New York that covered the basics that a founder needs to know about venture capital. From the definition of VCs to mechanics and bargaining, the discussion served as a primer for the second part of our series, “Selling to Fortune 100 Enterprises.” That session featured entrepreneurs from Bitium, Proofpoint, and Segment who spoke about how they did it: the tools and processes that they deployed, the design principles that they used, and the AWS services that allowed them to navigate the procurement maze and land big deals. But you need to learn to walk before you can run, which is why Drew is recapping his VC101 session for everyone who couldn’t attend in-person.

What is venture capital?

“Venture capitalist” is a job. Venture capitalists get paid by others to do this job, and while it’s a pretty great job, it’s important for anyone interacting with a venture capital firm to understand the basic mechanics and incentives that shape how the industry functions.

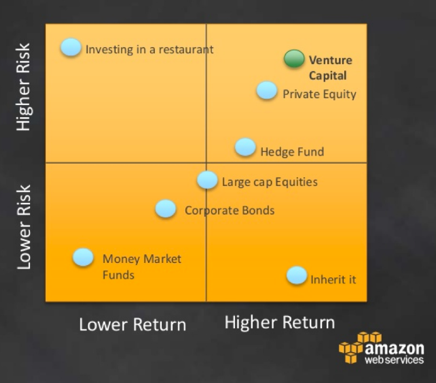

Venture capital is a form of private equity. While there are many differences within the industry, both venture capital managers and private equity managers strive to achieve very high returns in a relatively short period of time.

Venture capitalists are professional money managers. They are paid to manage money for clients. Their goal is to return investors a multiple (e.g. 2x, 3x etc) of the capital they are provided by their investors. For many VCs, investing in technology and innovation is the vehicle that they use to attempt to achieve this goal. VCs are willing to invest in high-risk businesses because of the potentially high reward that can be achieved by taking on this risk.

Therefore, not all businesses should raise venture capital. You should always consider all financing options and find the best fit for your needs based on your planned growth rates and, most important, the ultimate goal that you have for your business.

The theory of venture capital

Venture capital typically uses a portfolio approach to capture a distribution of probabilities. Venture fund returns are not driven by the “average” outcome of the portfolio, but rather by the significant outliers. Fred Wilson, of Union Square Ventures, states, “I’ve said many times on [this blog] that our target batting average is ‘1/3, 1/3, 1/3,’ which means that we expect to lose our entire investment on 1/3 of our investments, we expect to get our money back (or maybe make a small return) on 1/3 of our investments, and we expect to generate the bulk of our returns on 1/3 of our investments.”

The reality is that most startups fail. For VCs to be successful, they must identify “home runs.” The venture business is driven by these outliers. And truly successful VCs don’t just identify the home runs, they identify the grand slams. This is shown in the data: funds that have returned more than 5x the capital provided to them by their investors almost always tend to show a high concentration of these “grand slams”. In fact, these exceptionally high returning funds have portfolios that consist of almost 20% of deals that exceed 10x on the capital the fund invested. These are the individual “grand slams” (10x) that drive the overall fund return (5x).1 These “grand slam” investments determine whether a VC is successful. VC is about the wins, not the losses.

The venture capital bargain

If you are the founder of a startup and want to raise venture capital, you need to understand the deal that you will strike with a VC when you accept an investment. In particular, you need to understand what you will give up.

First, you give up absolute authority and control. While most VCs don’t meddle in a company that performs according to plan, you likely will add these investors to your Board of Directors, where they will be able to wield influence (usually more often in bad times, but not exclusively). Remember, they have a portfolio of companies and a set of investors, just like you do. Their incentives won’t—and shouldn’t—always align with yours.

Second, you give up a degree of ownership, also known as dilution. Typically, a VC that invests in a seed or Series A deal (early stage) wants to own 20–30% of your company. This allows them to maintain a reasonable ownership stake in the likely event that you decide to raise more capital. As you raise more, they also get diluted, reducing overall ownership (often, investors in early rounds also participate in future rounds, using what is called their Pro Rata right, but let’s not get distracted). At the time the company achieves a liquidity event (for example, the company is sold or goes public), they might own only 2% or so.

Last, you give up preference (which we discuss in more detail at the end of this post). That means that even though your blood, sweat, and tears have gone into this (and maybe some of your own capital or capital from your friends and family), VC investors with a preference will almost always get their money back, before you see any returns. This preference is important to understand as you think about how you will fare in the event of the hallowed IPO or acquisition.

You give this stuff up for a reason, though. You give up (some) control, preference, and ownership in exchange for significant capital that you could not raise anywhere else. Additionally, you gain the experience of the investors who are now working with you to achieve the best outcome.

Understanding these three principles is key to understanding the bargain of venture capital.

How venture capitalists make money

Now that we have covered how VC funds think about investment returns, you need to understand how venture capitalists—the actual individuals you meet or who sit on your board—get paid. In particular, you should be aware of two mechanisms: management fees and carried interest.

Management fees are fees paid by the investors of the VC fund. This fee is similar to what you might pay when you invest in a mutual fund or would pay to a professional money manager who manages your stocks and bonds. It is typically in the range of 1.5–2.5% annually of the funds managed, and is paid quarterly. The fee is paid independent of investment success. That said, the fee will decrease over the lifetime of the fund as the focus of the fund shifts from making new investments to harvesting returns on the investments made.

The second way VCs make money—and the one that generally gets a bulk of the attention—is carried interest, often referred to as carry. Carry is the share of the profit that the VC fund keeps. That is, once a VC fund has returned 100% of the capital provided back to investors, the VC fund begins to participate in a share of the profits above that 100% of capital returned. Typically, carry is pegged at 20% of the profits. Carry is a tricky business, though, as it is a fund-wide return that relies on grand slams to make up for complete losses elsewhere in the portfolio. Furthermore, not all members of a VC fund participate equally in receiving a portion of the carry. For younger folks at VC firms, “achieving carry” is a very big step up in the world.

Roles and responsibilities of a VC team

Speaking of the different members of a VC team, you should know the roles of the people you talk to when engaging a VC fund. It will help you craft your discussion to get the optimal result. Plus, it will help you understand their power to influence decisions within the firm.

The first chapter of Brad Feld’s and Jason Mendelson’s book, Venture Deals, does a wonderful job of outlining the different roles within a VC firm. I’ve borrowed heavily from that book in my descriptions of VC roles below (Mendelson, 2013):

- Analysts – Generally very smart people with limited power and responsibility. They usually are recent graduates from college, and they typically do a lot of the important work that no one else wants to do or has the time to do, such as crunching numbers and writing memos.

- Associates – Typically not deal partners, but they support one or more deal partners, usually a General Partner or Managing Director. They have a wide variety of responsibilities including scouting new deals, helping with due diligence, and writing internal investment memos.

- Sr. Associates/Principals – The next generation of Managing Directors. They are junior deal partners. They typically have some limited deal responsibility, but also often require support from a Managing Director. Typically they don’t make final decisions. That’s usually left to the Investment Committee, comprised of GPs and Managing Directors.

- Managing Directors/General Partners – The most senior people in the firm. These folks are the leaders of the firm. They approve all investments and sit on the boards of companies.

- Others: EIRs, Venture Partners, Operating Partners – These titles can mean a variety of things depending on the firm and the individual who holds the title. In general, these folks either are responsible for assisting the portfolio companies post-investment (Operating Partner) or they are part-time affiliates of the fund who incubate their own startup idea (EIR) or provide more deal flow to the VC fund (Venture Partner).

Deal sourcing

Venture capitalists typically look at 1000s of deals per year and invest in a small minority of these opportunities (approximately 1–4% of these deals, depending on the strategy of the fund). So, where do all these deals come from? “Deal flow,” the colloquialism often used to describe the volume of deals that a VC reviews, comes from a variety of sources. But the most valuable deal flow often comes from fellow VCs, founders, or other parts of an investor’s network who can pass along reliable, well-vetted, and well-accustomed opportunities.

Some VC firms use cold calling or outbound deal flow tactics, but the vast majority rely on warm leads sent by colleagues, friends, and former business partners. In fact, some VCs meet only with companies where the founder was introduced by another VC or from a founder that the investor has already worked with in the past. Some VCs won’t look at deals with a first-time founder. Some look at deals only if the founding team is from a certain school, or has a pedigree from certain technology companies. And, of course, some VCs ignore all these policies. The point is that the value of a VC is often equivalent to the reach and extent of their network of collaborators willing to send them investment opportunities that they know will align with the investment parameters of the VC fund.

Why venture capitalists invest at different stages

VC funds invest at different stages of a company’s lifecycle. Some focus only on “early stage investing,” while other focus only on “late stage.” Others focus on all stages, often referring to themselves at “stage agnostic.” Broadly speaking, each stage of investment—early, mid, or late—can be defined by the different type of risk associated with the business at the stage in their maturation. In addition to risk, investors at different stages also tend to look at different metrics, or, in the absence of metrics, the traits of a business to justify an investment.

The type of risk associated with early stage investing is what is called ideation and/or product market fit. Will the service or product you are selling have a real market? Or is what you have built really just a solution looking for a problem? Early stage investors typically focus on the founding team and their pedigree as well as acumen and drive as parameters for justifying an investment because there is little else to go on at this point in the business. Early stage investors generally ask themselves, “Can this product or service solve a big problem, and is this the right team to build the product or service?”

The type of risk associated with mid-stage investing (known as “traditional” VC investing only a few years ago) is about gaining traction and creating a business that can successfully scale to reach the broadest markets possible. At this stage, companies typically raise capital to support growth in Sales & Marketing spend and hiring. While early stage investors focus on getting the fire started, mid-stage investors tend to invest to help the company “pour more gas on the fire” (another colloquialism you will hear plenty). Mid-stage VCs are usually more focused on the core team—not just the founder—and the quality of the team being built to help achieve the scale that they want.

Finally, the type of risk associated with late-stage investing is best described as exit risk. While early stage and mid-stage are focused on creating the foundations of the company, and then rapidly scaling the business off of those foundations, later-stage investors are more focused on how you can monetize the business, through either a sale or an Initial Public Offering (IPO). Valuation and deal structure is always important at any stage, but they become the primary drivers of the return at the later stage. Investing in a company at a $20 MM valuation with the goal of growing the business to a multiple of that is far different from investing in a company at a $500 MM valuation and having a good understanding of what type of pricing the company could likely get at an IPO. Late-stage investors spend much more time thinking about IPO windows (periods of time when going public is more conducive) and the cash balances of potential acquirers than either early or mid-stage investors.

The ABCs of VC funding

As I mentioned, there are different stages at which investors invest. Most people are familiar with terms such as seed or Series B, but many don’t quite understand what those terms actually mean. To be fair, these terms—particularly seed—are constantly redefined or orphaned, and many folks just use them to suit their own needs. But there is some logic to the ABCs of VC.

In general, VC funding follows a Last in, First out (LIFO) principle. Those who invest their money last into a company will typically receive their money back first, before anyone else (i.e., before those who invested earlier). This is not always the case, but a good rule of thumb. That means that all investors in a company ARE NOT EQUAL. Shares issued to VC investors are typically preferred securities. This means exactly what it sounds like: the securities have preference over the securities that were issued before. For example, an investor who invests in the Series B of a company will receive an allotment of Series B Preferred Stock, representing their ownership of the company. These Series B preferred stock will generally have “preference” over the Series A Preferred stock holders (who in turn have preference over common stockholders, who have no preference at all).

Seed, Series A, or Series B and so on can be good indications of the stage of a company (although they also can be misleading), but the truth is that the reference is more to the preference of the holders of the securities. There are other important concepts, such as liquidation preference, that relates to this idea, but I will cover that in subsequent posts.

Conclusion

Venture capitalists have a job to do, just like everyone else. Yes, it’s a pretty cool job, but a job nonetheless. The goal of all VCs is to generate returns through liquidation events (and with all the talk about valuations in the news these days, it’s easy to forget that a valuation means nothing in terms of actual returns until the company achieves a liquidity event).

I hope this post has helped to expose some of the basic functions, mechanics, and, important, incentives as to why VCs do what they do and how they do it. If you are a founder of a company who plans to raise or has already raised venture capital financing, you don’t have to be an expert in the ins-and-outs of venture capital. However, it’s helpful to have a solid understanding given the potential impact on your ultimate success and achievements, both financially as well as personally.

We can help: AWS Activate

AWS Activate is a program designed to provide your startup with the resources you need to get started on AWS. All startups can apply for the Self-Starter Package. We also have custom Portfolio and Portfolio Plus packages for startups in select accelerators, incubators, Seed/VC Funds, and startup-enabling organizations.

Portfolio Package

The Portfolio Package is designed for startups in select accelerators, incubators, Seed/VC Funds, and other startup-enabling organizations. If your startup qualifies for a Portfolio Package, you can receive up to $15,000 in AWS Promotional Credit and other benefits. Ask your program director for more information about how to apply.

Portfolio Plus

If your startup qualifies for a Portfolio Plus package, you can receive up to $15,000 in AWS Promotional Credit for 2 years or $100,000 for 1 year and other benefits. Ask your program director for more information about how to apply.

To learn more about corporate VCs and the other flavors of VCs, and to obtain links to blogs, books, and newsletters from prominent thought leaders, check out Russ’s slideshare deck, “VC 101: How, What & Why VCs Do What They Do.”

1Chris Dixon, Andreessen Horowtiz Blog Post, http://cdixon.org/2015/06/07/the-babe-ruth-effect-in-venture-capital/