AWS Public Sector Blog

The future of money is digital: How the cloud can deliver solutions for central bank digital currencies

Increasingly, central banks want to answer practical questions and make the technology choices involved to deliver a central bank digital currency (CBDC). They need a solution that delivers on their missions and meets the performance criteria required to support a stable monetary and financial system.

To help organizations understand available technology options and see how cloud services can enable optimal solution designs, Amazon Web Services (AWS) authored a two-part whitepaper. Part one is, “Central bank digital currency: Objectives and architectural considerations,” and part two is, “Central bank digital currency: Technology options and performance criteria.” The report offers guidance and best practices surrounding CBDC objectives, architectural considerations, technology options, and performance criteria. Here are some of the highlights.

Identifying objectives before design

The design of a CBDC should depend on the organization’s objectives. One common objective is to reduce reliance on existing payment methods, increase competition, and provide additional resilience to the payments system. Another is to encourage innovation that delivers new services in a digital economy, such as programmable money, to enable conditional payments and micro-payments. Others include increasing financial inclusion to the underbanked, improving transparency into and traceability of cross-border payments, and detecting and preventing unlawful activities.

Architectural considerations based on objectives

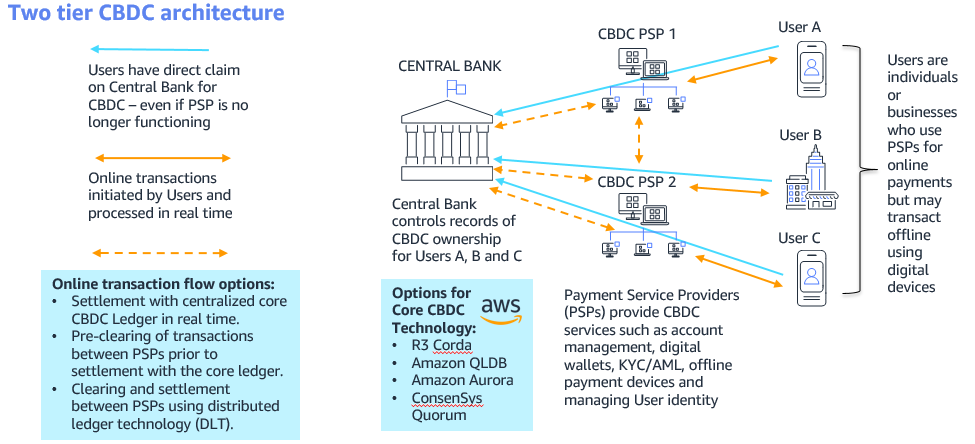

One way to encourage innovation and competition is to adopt a two-tier architecture in which CBDC users don’t have direct contact with the central bank but instead access funds and transact through payment services providers (PSPs), such as commercial banks.

Other aspects of architectural design include: whether a solution should be token-based, where users don’t have to provide their identity, or account-based, requiring them to prove they own the account; offline capability, which could allow users to make low value transactions anonymously, like cash; clearing and settlement models; network architecture options; and the interoperability between PSPs and their various roles.

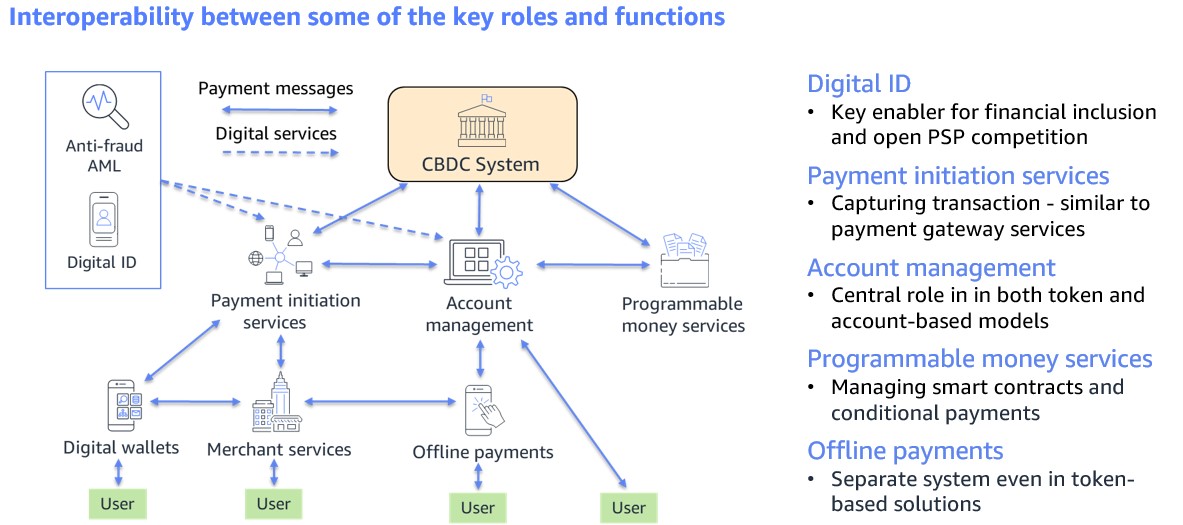

Interoperability between some key CBDC roles and functions

Exploring technology options

A key question is which technology to use to store the ownership of CBDC and process transactions. The two most common technology alternatives are distributed ledgers using blockchain technology and centralised databases.

Each of these has advantages and disadvantages in terms of their technical performance. Blockchain technology has features such as immutable records and support for smart contracts. It also provides the ability to create a system where each participant has a share of operational control. Commercial banking systems use centralised ledgers widely today, and there are established solutions proven capable of operating at scale. In both of these technology alternatives, organizations are increasingly adopting cloud services like Amazon Aurora to reduce costs and access advanced features or Amazon Quantum Ledger Database (Amazon QLDB), which provides immutability.

Key technical performance criteria

Performance metrics such as security, throughput, transaction time, and resilience are of paramount importance in designing a CBDC system. A centralised database has a limited footprint, which means fewer security vulnerabilities and fewer cyberattack entry points than a blockchain solution. In terms of throughput and transaction time, the number of messages participants must exchange to process a transaction and the complexity of the steps the system follows for settlement can be a disadvantage for some blockchain solutions

For enhanced availability and resilience, centralised databases delivered on the AWS Cloud have the advantage of multi-Region disaster resiliency. Achieving such resilience with a blockchain solution can be more complex, but if architected correctly, they can continue operating in the event of a disaster, which only affects part of the network and could make them more resilient than their centralized database counterparts.

Further work is required to address blockchain solution issues and their support to general-purpose CBDC solutions, but there is potential given the rapid development in blockchain technology and innovative implementation approaches.

The role of cloud

For CBDC solutions to be successful, they must provide a robust and usable infrastructure for executing payments. The scalability and performance of AWS can help central banks deliver and manage comprehensive CBDC solutions that are secure from sophisticated threat actors and human error, are available and resilient against disasters, scale to peak demand, and support interoperability, flexibility, and adaptability.

AWS can also support developing proofs-of-concept, running pilots and to test data analytics use cases, like gaining insights into economic conditions or enhancing capabilities to detect and prevent fraud and money laundering.

To learn more and dive deep on solutions for CBDC, download part one, “Central bank digital currency: Objectives and architectural considerations,” and part two, “Central bank digital currency: Technology options and performance criteria.”